The Washington D.C. real estate market has long been shaped by its status as the nation’s political and economic hub. Between 2023 and 2025, the region faces a unique mix of challenges and opportunities, driven by fluctuating interest rates, shifting demand patterns, and evolving federal policies. This article breaks down current trends, forecasts for 2024 and 2025, and actionable insights for buyers, sellers, and investors navigating this dynamic market.

2023 Market Snapshot: Key Data and Trends

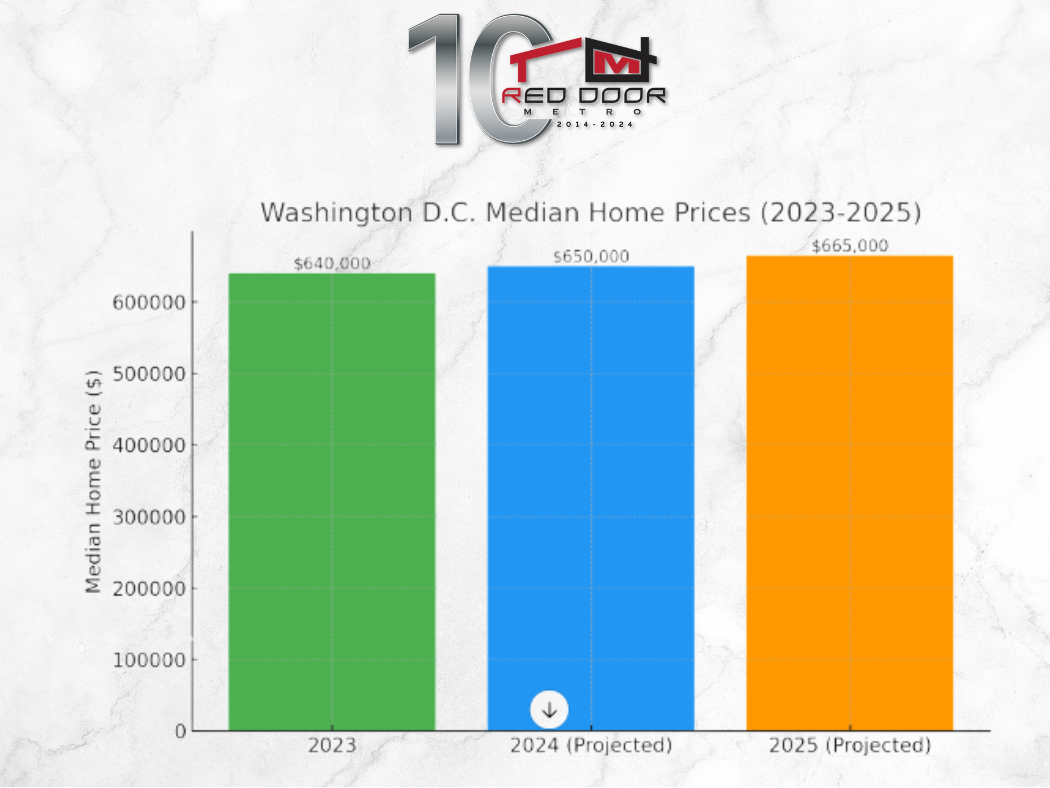

- Median Home Prices: As of Q4 2023, the median home price in Washington D.C. stands at $640,000, a modest 2.8% increase from 2022. While growth has slowed compared to the 8% surge in 2021–2022, prices remain elevated due to limited inventory.

- Inventory Challenges: Active listings are down 18% compared to pre-pandemic levels, with only 1.7 months of supply—far below the 6-month benchmark for a balanced market. Single-family homes are especially scarce, driving competition in neighborhoods like Chevy Chase and Capitol Hill.

- Interest Rates: Mortgage rates peaked at 7.8% in October 2023 (up from 3% in 2021), dampening buyer activity but not halting it. D.C.’s stable job market—fueled by federal agencies, contractors, and nonprofits—has kept demand steady.

- Rental Market: Average rents hit $2,450/month in 2023, making D.C. the 6th most expensive rental market in the U.S. Vacancy rates tightened to 4.3% as high mortgage rates forced many residents to delay homebuying.

2024 Forecast: Moderating Prices and Inventory Gains

1. Home Prices Stabilize

Economists project a 1–3% price increase in 2024, with growth concentrated in single-family homes and townhouses. Condo prices, however, may dip another 1–2% due to oversupply in downtown areas like NoMa and Southwest Waterfront.

2. Mortgage Rates Decline Gradually

The Federal Reserve’s anticipated rate cuts in late 2024 could push mortgage rates down to 6.5–6.8%, reviving buyer demand. First-time buyers may re-enter the market, particularly for condos and “starter homes” under $500,000.

3. Inventory Slowly Improves

New construction permits rose 12% in 2023, signaling a potential inventory boost in 2024. However, most new units are luxury condos or multi-family buildings, doing little to ease the shortage of affordable single-family homes.

4. Federal Return-to-Office Mandates

With federal agencies requiring 3–4 days in-office per week, demand for walkable urban neighborhoods (e.g., Dupont Circle, Navy Yard) will rise. Suburban markets like Arlington and Bethesda may see slower growth as hybrid workers prioritize shorter commutes.

2025 Predictions: A Shift Toward Balance

1. Price Growth Normalizes

By 2025, home price increases are expected to stabilize at 2–4% annually, aligning with historical norms. A surge in new multi-family housing developments could ease pressure on rentals, with vacancy rates rising to 5–6%.

2. Interest Rates Dip Below 6%

If inflation continues to cool, mortgage rates could fall to 5.75–6.25% by late 2025, unlocking pent-up demand from mid-tier buyers. Refinancing activity may also rebound.

3. Suburban Markets Rebound

Areas near Metro expansions—such as the Silver Line’s Phase II (Ashburn, Reston)—will attract buyers priced out of D.C. proper. Communities with mixed-use developments (e.g., Tysons, Silver Spring) will thrive.

4. Policy Impacts

- Affordable Housing Initiatives: D.C.’s $400 million investment in affordable housing (2023–2025) may add 3,000+ units, targeting neighborhoods like Anacostia and Deanwood.

- Short-Term Rental Regulations: Stricter Airbnb rules could redirect investor focus to long-term rental properties.

Neighborhoods to Watch (2023–2025)

- Anacostia: Median prices ($460,000) remain 30% below the citywide average, with revitalization projects like the 11th Street Bridge Park driving interest.

- Petworth: Demand for single-family homes (median $765,000) persists, bolstered by new retail and the Georgia Avenue corridor redevelopment.

- Congress Heights: Investors are eyeing multi-family properties here, with prices 20% lower than the D.C. average.

- Georgetown: Luxury sales dominate, with historic townhouses averaging $3.2 million.

Actionable Strategies for Market Participants

For Buyers:

- Prioritize Pre-Approvals: Competition remains fierce, especially for homes under $800,000.

- Consider “Transitional” Areas: Neighborhoods like Brookland and Brightwood Park offer relative affordability with growth potential.

- Lock in Rates: If rates drop below 6.5% in 2024, act quickly to refinance later.

For Sellers:

- Stage for Hybrid Work: Highlight home offices, high-speed internet, and proximity to transit.

- Price Realistically: Overpriced homes linger 40% longer on the market, per Bright MLS data.

For Investors:

- Target Multi-Family Units: Demand for rentals will stay strong through 2025.

- Watch for Policy Shifts: Tax incentives for affordable housing developers may emerge in 2024.

For Renters:

- Negotiate Lease Terms: Landlords are offering concessions (e.g., 1–2 months free) to fill luxury units.

- Explore Rent-to-Own Programs: Some builders are offering flexible pathways to homeownership.

Long-Term Risks and Opportunities

- Risks:

- A recession could slow federal hiring and dampen demand.

- Prolonged high interest rates (>7%) may price out first-time buyers.

- Opportunities:

- D.C.’s population growth (projected +5% by 2025) will drive housing demand.

- Federal infrastructure spending could boost construction and transit-oriented development.

Conclusion

The Washington D.C. real estate market is poised for gradual stabilization between 2023 and 2025, with moderating price growth, improving inventory, and declining mortgage rates. While challenges like affordability and supply shortages persist, strategic buyers, sellers, and investors can capitalize on emerging trends in urban revitalization, suburban expansion, and policy-driven opportunities. Staying informed—and agile—will be key to success in this evolving landscape.

Data sources: Bright MLS, U.S. Census Bureau, D.C. Office of Revenue Analysis, Federal Reserve Economic Data (FRED), Urban Institute.

FAQs

-

How have home prices in Washington D.C. changed recently?

- As of February 2025, home prices in Washington D.C. have increased by 11.5% compared to the previous year, with a median sale price of $657,000.

-

What is the average time a property stays on the market?

- On average, homes in Washington D.C. are on the market for 80 days, up from 63 days last year.

-

How has the number of home sales changed over the past year?

- In February 2025, 485 homes were sold, a slight decrease from 493 sales in the same month last year.

-

What are the projections for home sale prices in 2025?

- The median home sale price in the D.C. region is expected to rise by 4.7%, from $609,700 in 2024 to $638,310 in 2025.

-

Is there an expected change in the number of home sales?

- Yes, home sales are projected to increase by 7.9%, from 49,630 in 2024 to 53,550 in 2025.

-

How is housing inventory expected to change?

- The number of active listings is anticipated to grow by 14%, from 5,710 to 6,507 by the end of 2025.

-

What impact could federal budget cuts have on home prices?

- Proposed budget cuts by the Department of Government Efficiency (DOGE) may lead to increased housing inventory, potentially reducing property prices and shifting leverage to buyers.

-

How are tariffs affecting construction costs in D.C.?

- Tariffs on materials like steel and aluminum have raised construction costs, leading to budget increases and potential delays in new projects.

-

What trends are observed in the commercial real estate sector?

- The office market has softened, with vacancy rates rising to 17.1% by the end of Q2 2024, a trend expected to continue in 2025.

-

Which neighborhoods are experiencing significant price changes?

- Neighborhoods like Georgetown and Capitol Hill have seen varying trends, with median list prices and days on market differing across areas.

-

How are mortgage rates influencing buyer behavior?

- Fluctuations in mortgage rates are significantly impacting buyer activity, with potential rate drops expected to increase demand.

-

What is the current state of the rental market?

- Rental investments remain attractive, with a focus on eco-friendly and sustainable housing options gaining prominence.

-

Are there any signs of gentrification in specific neighborhoods?

- Yes, the emergence of gray-painted houses is often associated with gentrification, reflecting demographic shifts in areas like Washington D.C.

-

How is the luxury home market performing?

- The luxury home market is experiencing a surge, with high-profile buyers and increased competition leading to record sales and price hikes.

-

What are the expectations for new housing developments?

- New buildings and communities are expected to come online in 2025, with a focus on sustainability and technological advancements.

-

How is the work-from-home trend affecting the market?

- A decline in remote work is anticipated, with federal workers expected to return to offices, potentially influencing housing demand in urban areas.

-

What are the key factors influencing the D.C. housing forecast?

- Economic opportunities, political influence, and cultural richness continue to make Washington D.C.’s real estate market a standout in the U.S.

-

How are sustainability trends impacting real estate?

- There’s a growing emphasis on eco-friendly and sustainable housing, with new developments focusing on green building practices.

-

What demographic shifts are affecting the housing market?

- Demographic changes, including shifts in population dynamics, are influencing housing demand and neighborhood compositions.

-

How can buyers and sellers navigate the current market?

- Staying informed about market trends, mortgage rates, and neighborhood developments is crucial for making well-informed real estate decisions in 2025.